BaaS infrastructure

UK coverage

EU coverage

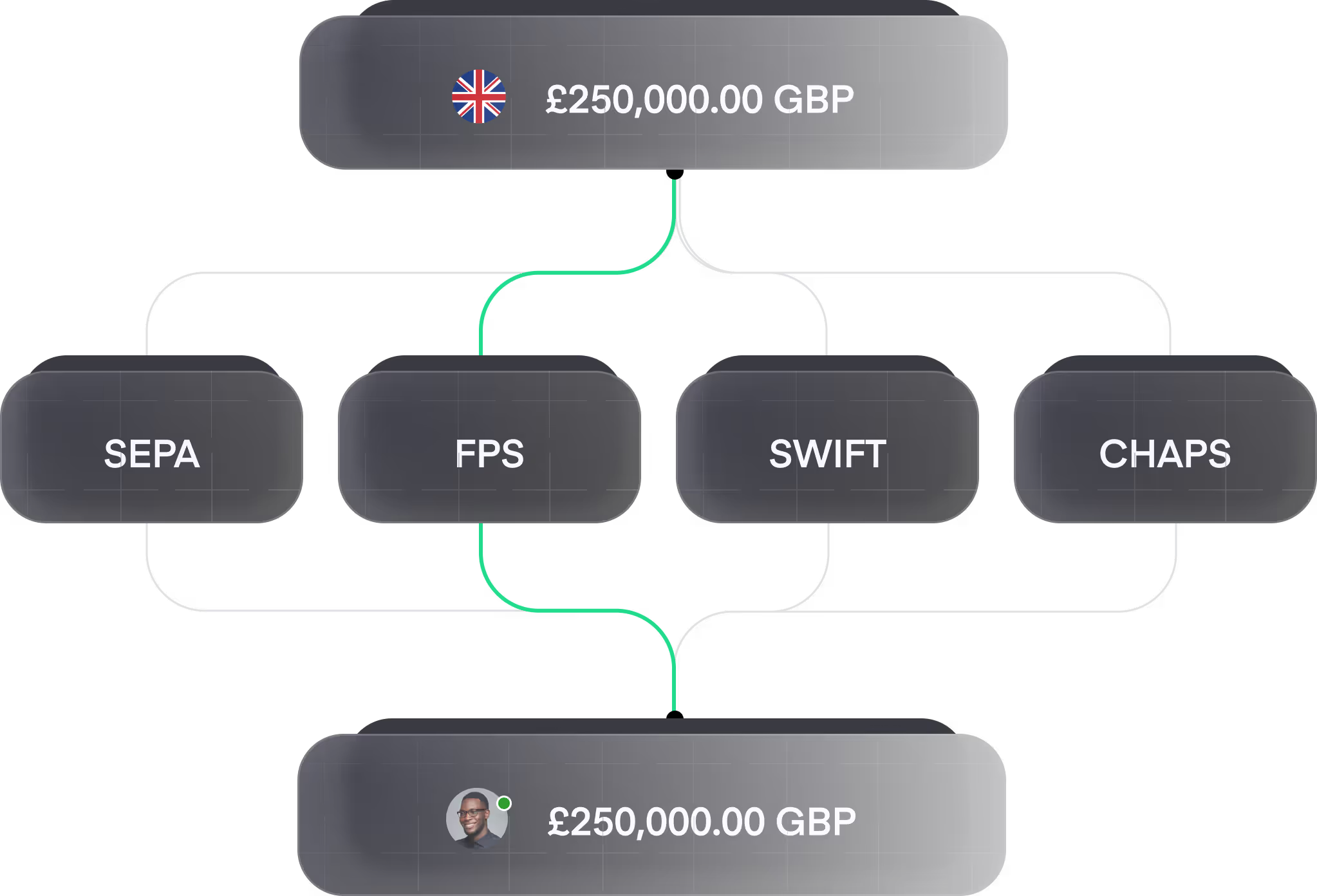

Payments

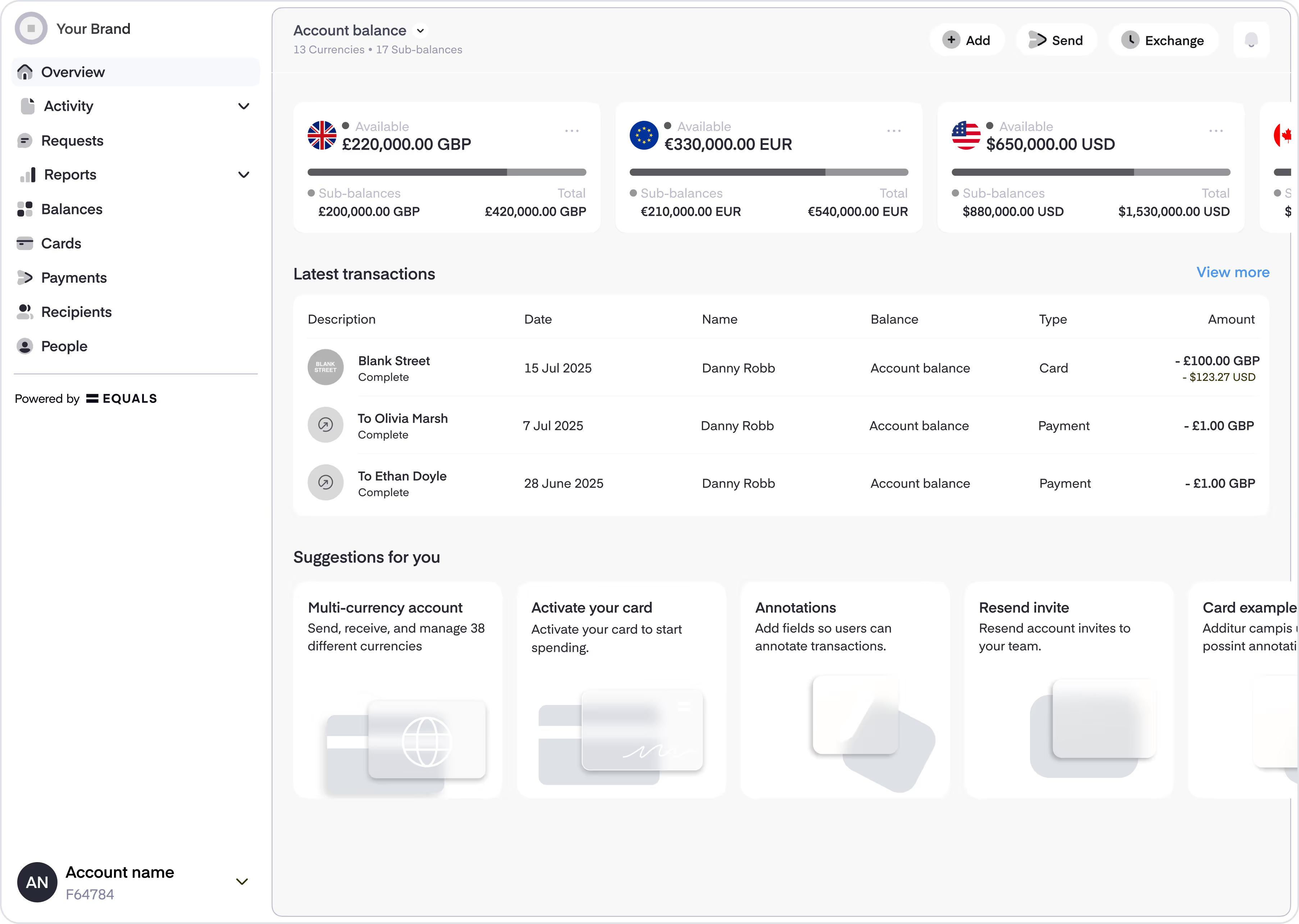

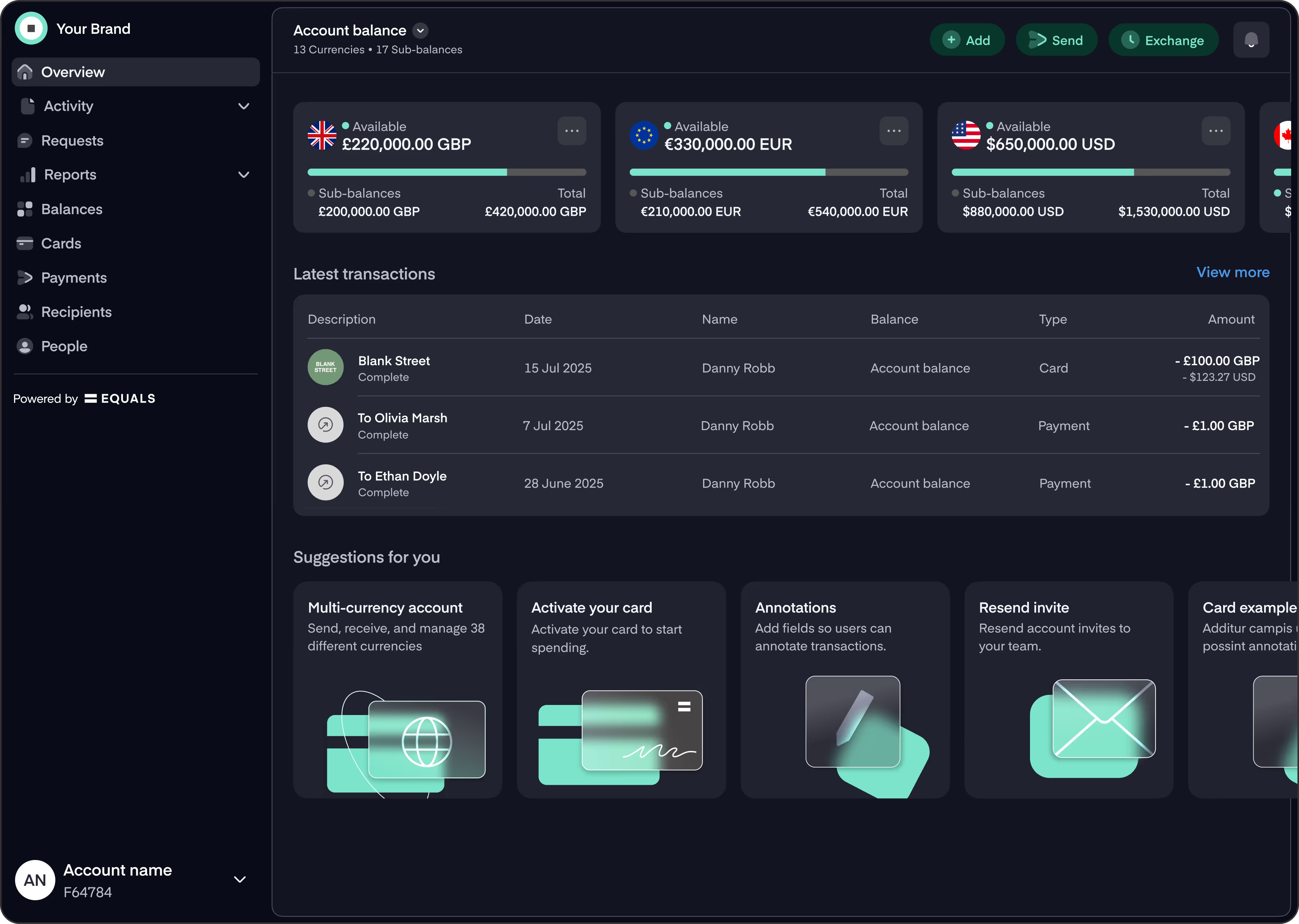

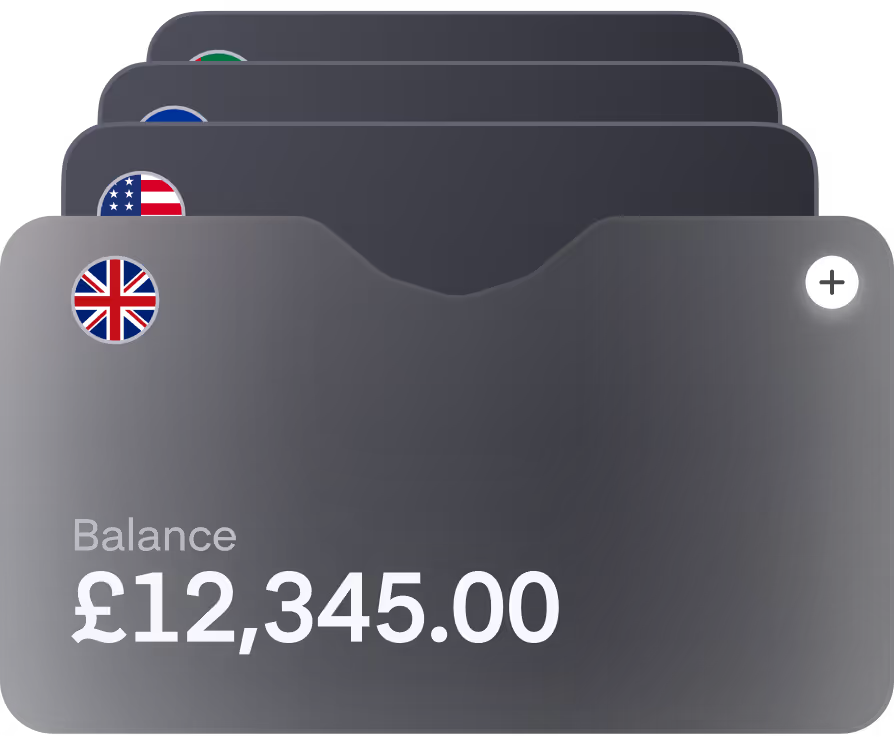

Multi-currency IBAN

38 currencies

23 currencies

Payment rails

UK FPS, CHAPS, SEPA CT, SEPA Instant, SWIFT

SEPA CT, SEPA Instant, SWIFT

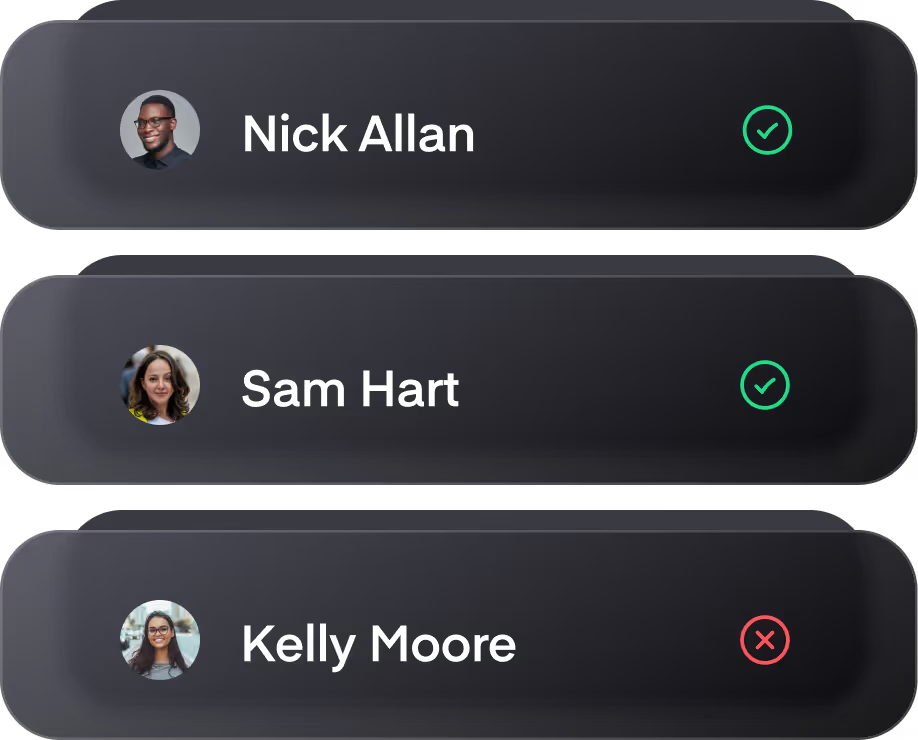

Confirmation of Payee (CoP)

Verification of Payee (VoP) - in EU

Open Banking capabilties

Coming soon

Cards

BIN sponsorship

Card schemes

Visa, Mastercard

Visa, Mastercard

Card types

Physical, virtual, tokenised

Physical, virtual, tokenised

Mobile wallet(s)

Apple Pay, Google Pay, Samsung Pay

Apple Pay, Google Pay, Samsung Pay

Tech

White label mobile app

White label web app

API

Customer & servicing

Agents model

Full-service model

White label model

Customer servicing

Know Your Customer (KYC)

All fees are custom to banking as a service requirements.